Atradius Atrium

Get direct access to your policy information, credit limit application tools and insights.

United States

United States

Australia

Australia

Austria

Austria

Belgium

Belgium

Brazil

Brazil

Bulgaria

Bulgaria

Canada

Canada

China

China

Czech Republic

Czech Republic

Denmark

Denmark

Finland

Finland

France

France

Germany

Germany

Greece

Greece

Hong Kong SAR

Hong Kong SAR

Hungary

Hungary

India

India

Ireland

Ireland

Italy

Italy

Japan

Japan

Lithuania

Lithuania

Mexico

Mexico

Netherlands

Netherlands

New Zealand

New Zealand

Norway

Norway

Poland

Poland

Portugal

Portugal

Romania

Romania

Singapore

Singapore

Slovakia

Slovakia

Slovenia

Slovenia

Spain

Spain

Sweden

Sweden

Switzerland

Switzerland

Turkey

Turkey

United Arab Emirates

United Arab Emirates

United Kingdom

United States

United Kingdom

United States

Customer payment risks in business-to-business (B2B) trade across Asia appear to be edging higher. Survey data points to a recent rise in late payments, making cash flow less predictable, while higher bad debt write-offs are adding strain on working capital, putting pressure on liquidity, and making cash flow planning more challenging. To limit the impact of payment risks on the business and safeguard financial stability, companies surveyed across Asia are adapting how they manage trade credit policies in B2B transactions.

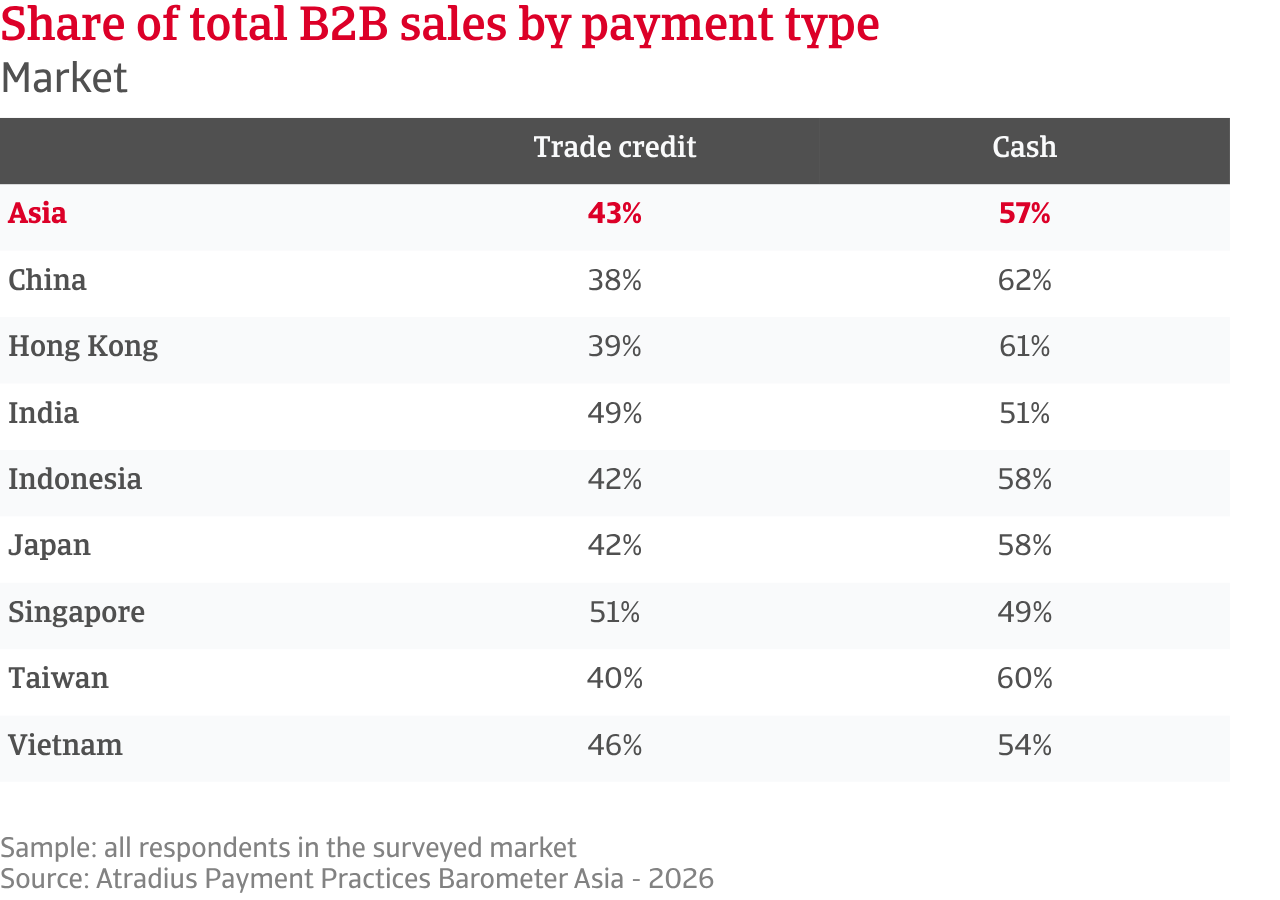

This is primarily reflected in how likely they are to offer trade credit to business customers. Data shows that an average of 43% of B2B sales in Asia are made on credit, with the remainder paid upfront. In an uncertain environment, companies adopt a cautious approach, balancing sales growth with liquidity protection. Construction firms, particularly mid-sized ones, rely more heavily on B2B trade credit, due to long project cycles and complex supply chains. At market level, Singapore records the highest share of credit-based B2B sales at 51%, reflecting its role as a regional and global trade hub. In contrast, China records the lowest, with companies relying more on alternative solutions such as supply chain finance. Recent increases in trade credit use, led by large industrial firms and markets such as Vietnam and Indonesia, reflect efforts to secure volumes and protect market share. Differences across markets point to varying risk appetite.

Payment policies among Asian suppliers confirm this cautious stance. Most businesses across the region set payment from B2B customers of up to two months of invoicing, with longer terms remaining limited. Smaller firms keep terms short to protect liquidity, while larger firms apply flexibility more selectively. Companies in Japan offer the shortest payment terms, while businesses in Vietnam stand out for offering the most lenient payment timelines across the region. Trend data shows that payment policies across Asia have remained broadly stable over the past months. However, large industrial companies, along with Vietnamese firms, stand out for their higher level of activity in shifting terms. They are more likely than their peers across Asia to extend payment timelines rather than shorten them.

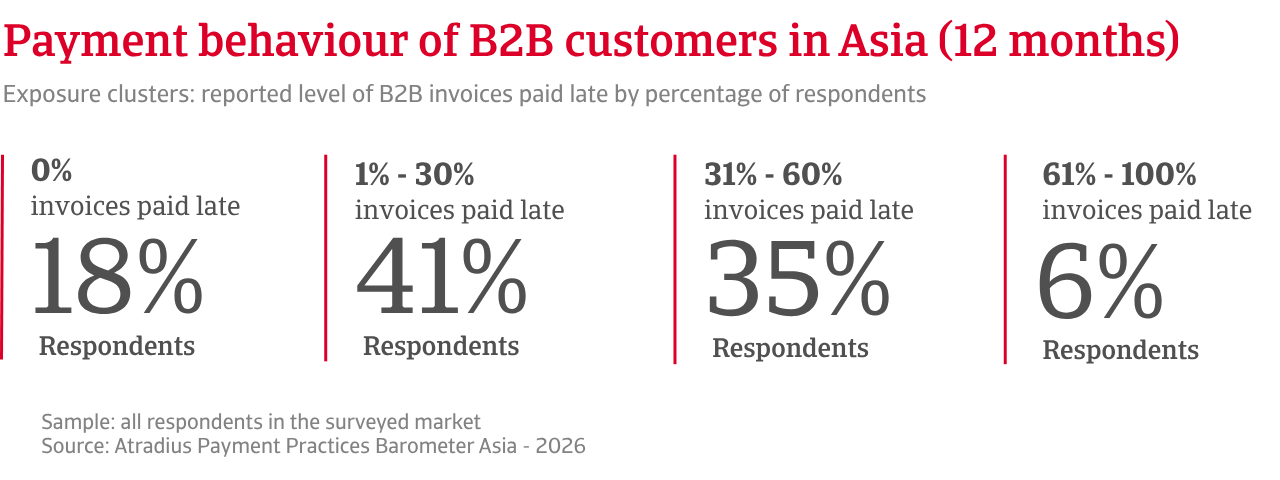

Despite tight control over trade credit policies in B2B transactions, customer payment risk remains widespread across Asia. More than 80% of suppliers report late payments, highlighting a clear gap between agreed terms and actual payment behavior. Overdue invoices account for nearly one third of B2B receivables, rising to around two in five among smaller firms in construction and trade. Indian companies are hit hardest by late payments, while Japanese firms stand out for the lowest exposure to delayed payments across the region. Trend data suggest that the share of overdue invoices has increased recently across Asia, reflecting a gradual weakening in payment discipline. This trend is most evident among businesses in the manufacturing sector, and at market level in Taiwan and Indonesia.

Customer cash flow stress is the main driver of delays across the region, according to survey data. Large industrial firms report this most often, as do businesses in Vietnam. Banking delays, as well as operational and administrative inefficiencies, also cause frequent delays across most markets. One in five suppliers across the region report that B2B customers often delay payments due to commercial frictions, such as delivery or quality disputes. Survey data also highlights that most overdue payments are settled within about one month past due, helping contain receivables build-up as well as sharp increases in Days Sales Outstanding (DSO). However, when receivables deteriorate, most often because they remain unpaid for longer periods or because the customer is no longer able to pay, they turn into credit losses, which appear widespread across Asia and on average affect between 1% to 5 % of B2B receivables across the region. Higher losses are more common among large construction and trade companies, as well as in markets such as China and India. Trend data show that credit losses have edged up in recent months across Asia. Increases are most often reported by manufacturing firms and, at market level, by companies in Hong Kong.

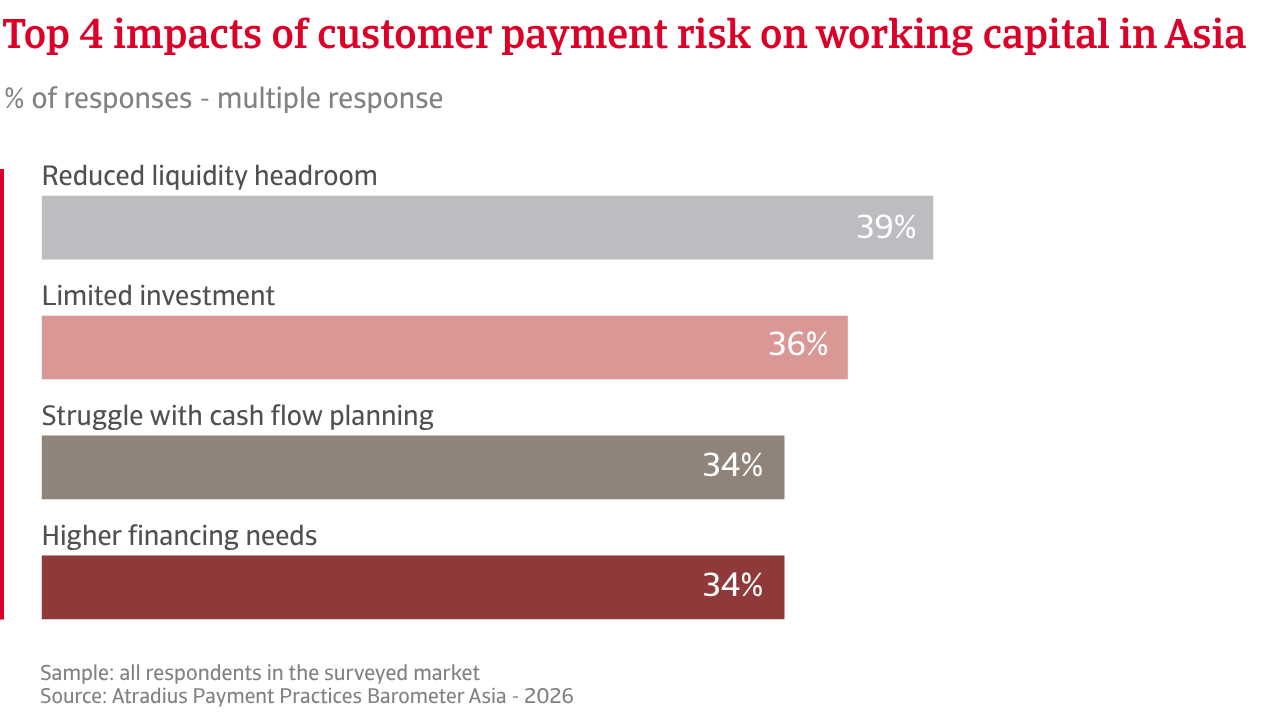

Within this context, most businesses report reduced cash available for operations, weaker cash flow planning, and limited investment. Nearly one third of firms face higher financing costs, while one quarter rely more on external funding. Many also delay their own payments, passing pressure along the supply chain. The impact of payment risk varies across business segments and markets, with industrial and trade firms among the most affected. At market level, liquidity pressure is most acute in Indonesia, cash flow planning challenges more evident in Vietnam, and investment constraints most acutely felt in China.

When asked about the tools and strategies used to mitigate customer payment risk, most businesses across Asia report relying mainly on internal measures. These include active credit management, such as checking customers, monitoring payments, and chasing collections. Requests for upfront payments are reported almost as often. Building bad debt reserves is used by just under one third of firms while a similar share use credit insurance, particularly mid-sized industrial companies and businesses in Vietnam and Indonesia. This positions it as a key external tool to protect against non-payment and support cash flow. Overall, firms take a layered approach to risk management, keeping close control of daily operations while using risk transfer solutions to deal with larger and less predictable losses.

Overdue invoices account for nearly one third of B2B receivables, rising to around two in five among smaller firms in construction and trade.

Early data for this year suggests insolvencies may have reached a turning point in several Asian markets, with the overall trend expected to ease through the remainder of the year. However, pressure persists in some sectors and markets highly exposed to global trade and cost volatility.

Against this backdrop, companies across Asia are almost evenly split between those expecting improvement in B2B customer payments in the months ahead and those anticipating deterioration. Trade firms are the most optimistic, while firms in industry, construction, and services remain more measured. Larger firms appear more confident than small firms, likely supported by stronger access to financing and more diversified customer bases. At market level, Vietnam stands out as the most optimistic, followed by India and Indonesia. In contrast, companies in Taiwan, Japan, and Hong Kong show more cautious sentiment, while firms in China and Singapore sit in the middle, expressing stronger uncertainty.

On insolvency risk, businesses across Asia are broadly divided, with near equal shares expecting a rise or stability, and few without a clear view. This highlights uncertainty about the strength of the recovery. Large industrial companies appear the most concerned about an upward trend in insolvencies in the months ahead, while construction, trade and services firms expect levels to remain broadly stable. At market level, Indonesia shows the most negative outlook, with a strong majority expecting insolvencies to rise. China and Taiwan also reflect high concern. By contrast, Hong Kong and Japan appear less concerned, with most firms expecting stability. Singapore and India sit closer to the regional average, reflecting an uncertain outlook. Survey data suggests that insolvency risks and profit expectations reflect a market where some firms expect to improve profitability through pricing, cost control, or efficiency gains, while others remain exposed to cost pressures, tighter financing, and weaker demand, increasing the risk of insolvency.

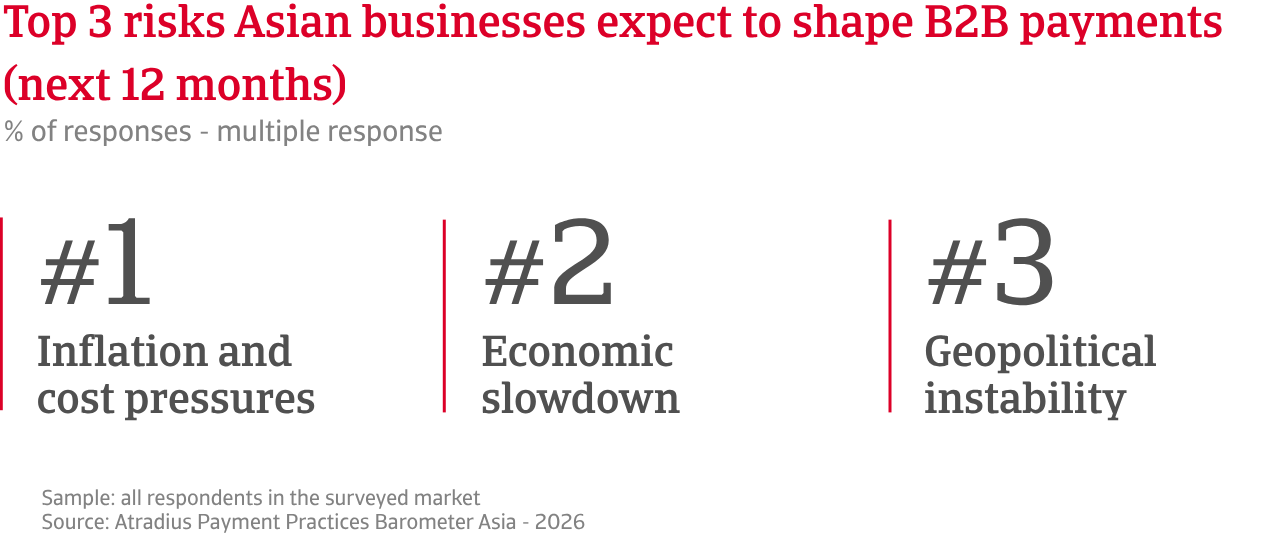

When asked about the main risks likely to disrupt B2B payment behaviour in the months ahead, views differ across business segments and markets, although inflation and economic slowdown prevail. Construction expects to face macroeconomic pressures, trade is concerned about commercial risks, while the services sector is sensitive to digital threats. Larger firms are concerned about financial risks, while smaller businesses are worried about operational threats such as cybersecurity and fraud. By market, Japan stands out as the most concerned market about economic slowdown, while Indonesia and Vietnam show heightened sensitivity to weakening demand. In contrast, inflation and cost pressures dominate in Taiwan, Hong Kong underscoring persistent cost burdens. In China, cybersecurity and fraud risks rank highest, while Vietnam stands out for supply chain disruption concerns.

For a full overview of the 2026 survey results for Asia, please download the regional report and the statistical appendix from the related documents section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.