Atradius Atrium

Get direct access to your policy information, credit limit application tools and insights.

United States

United States

Australia

Australia

Austria

Austria

Belgium

Belgium

Brazil

Brazil

Bulgaria

Bulgaria

Canada

Canada

China

China

Czech Republic

Czech Republic

Denmark

Denmark

Finland

Finland

France

France

Germany

Germany

Greece

Greece

Hong Kong SAR

Hong Kong SAR

Hungary

Hungary

India

India

Ireland

Ireland

Italy

Italy

Japan

Japan

Lithuania

Lithuania

Mexico

Mexico

Netherlands

Netherlands

New Zealand

New Zealand

Norway

Norway

Poland

Poland

Portugal

Portugal

Romania

Romania

Singapore

Singapore

Slovakia

Slovakia

Slovenia

Slovenia

Spain

Spain

Sweden

Sweden

Switzerland

Switzerland

Turkey

Turkey

United Arab Emirates

United Arab Emirates

United Kingdom

United States

United Kingdom

United States

Global insolvencies are forecast to rise by 3% in 2026. This represents a 6 percentage points upward revision compared to our October 2025 Insolvency Outlook. For 2027, we predict a 6% global decline.

The business climate remains vulnerable in 2026 as challenging economic conditions persist, including Covid-era debts, rising input costs and trade tensions. The crisis in the Middle East, and the associated increase in energy prices presents an additional headwind for companies. In our baseline scenario, shipping traffic through the Strait of Hormuz remains close to zero for a period of two months, after which it gradually normalizes. If the crisis in the Middle East drags on longer than we currently foresee, then the economic outlook and insolvency projections are subject to downward revision.

Looking ahead to 2027, we expect that companies will increasingly adapt to the new economic environment. As long as inflation remains relatively contained, there is still room for the Federal Reserve to lower the policy interest rate slightly in 2027. In the eurozone, the central bank is likely to see room to lower policy rates again. Together with a normalization in energy prices as shipping bottlenecks are resolved, this leads to an improved business climate and lower insolvencies.

On 28 February, the US and Israel launched a large-scale military campaign against Iran, targeting the regime's leadership as well as military and security infrastructure. Iran responded by launching ballistic missiles and drones at Israel and US bases and regional allies. It has also closed the Strait of Hormuz, a choke point for roughly one-fifth of global crude oil and seaborne gas flows. The developments have triggered a significant increase in global energy prices, with the oil price up by 55% since the start of the crisis and European gas prices up by 73%. In our baseline scenario, the Strait of Hormuz remains effectively closed until the end of April. Further assumptions are that attacks on Gulf infrastructure cause limited damage, and disruptions to the Strait of Hormuz will be gradually resolved from May onwards.

The drag of the Middle East crisis on global growth is estimated to equal 0.4 percentage points, leading to a 2.6% growth in 2026. This is just a notch above the growth we expected in our October 2025 Insolvency Outlook. If the disruption of trade flows through the Strait of Hormuz continues longer than expected or the damage to energy infrastructure is higher than predicted, the downward economic effects could be worse. Therefore, the risks for the global economy still lean to the downside.

The eurozone is expected to experience modest 0.8% growth in 2026, before rebounding to 1.5% in 2027. The eurozone will feel the negative effects of trade tariffs this year, as well as the disruption in gas markets that leads to higher energy prices and inflation. We expect that gas supply disruptions will push up inflation by 1.2 percentage points in 2026 compared to the pre-war baseline, bringing the inflation rate to 2.9%. The energy price rise will be the main channel, but it will feed through into the prices of other goods as well. Fiscal policy, mainly in the form of fuel subsidies and price ceilings, may help to cushion the worst impact. In the eurozone, countries in the south are demonstrating relatively strong GDP figures, driven by a growing tourism sector, labour market recovery and fiscal spending. Rising energy prices are a setback for Germany’s industrial sector, which was already struggling with tariffs and subdued foreign demand.

For the US economy, we predict a 2.4% growth in 2026 and 2.7% in 2027. For 2026, growth is revised upwards by 0.4 percentage points compared to October 2025, mainly due to stronger consumer spending and investment tailwinds from the AI boom. In February 2026, the US Supreme Court invalidated all tariffs implemented last year under emergency economic powers. However, the administration responded by pivoting to alternative legal authorities, introducing a uniform import surcharge. We estimate that the new effective tariff will be close to its previous level.

The US is comparatively resilient to the disruptions in energy markets that result from the Middle East conflict. The US is a net energy exporter and is not susceptible to the loss of LNG supplies from the Gulf. However, higher oil prices will still push up inflation in the US, since they directly pass through to consumer energy prices. US inflation is now expected to average 3.2% in 2026, 0.8 percentage points higher than previously expected.

Central banks must weigh the inflation shock caused by higher energy prices against the risk of a stagnating economy. In the US, the Federal Reserve follows a dual mandate of maximum employment and stable prices. Fed officials are still pencilling in a rate cut before the end of the year. This would bring the end-year policy rate to 3.5%. In contrast to the Fed, the ECB isn't starting from a restrictive stance, which constrains its flexibility to support the economy. Given the substantial inflationary shock in the eurozone, we even expect two rate hikes in June and July, as the ECB wants to keep inflation expectations in check and avoid the risk of acting too late. This would bring the end-year policy rate in the eurozone to 2.5%. Forecasts for mid-2027 suggest a return to a neutral rate of approximately 2% as energy prices are expected to normalize.

In the short term, companies may be impacted by more restricted access to credit due to ongoing economic uncertainty. Credit standards for loans to companies in the eurozone already tightened in Q4 of 2025. This was driven by perceived risks to the economic outlook as well as the lower risk tolerance displayed by banks, signalling a higher degree of risk aversion. In the US, banks also reported tighter lending standards for commercial and industrial loans to firms of all sizes. In the eurozone, central bank policy rate hikes may contribute to a further tightening of credit conditions in the rest of 2026. In 2027, however, we think that the central bank will again see room to lower interest rates. US bank lending standards are expected to remain broadly unchanged over 2026, with downside risks coming from both policy uncertainty and energy prices. The good news for companies is that they have already benefited from the monetary easing of 2024 and 2025, which provides them with some breathing space.

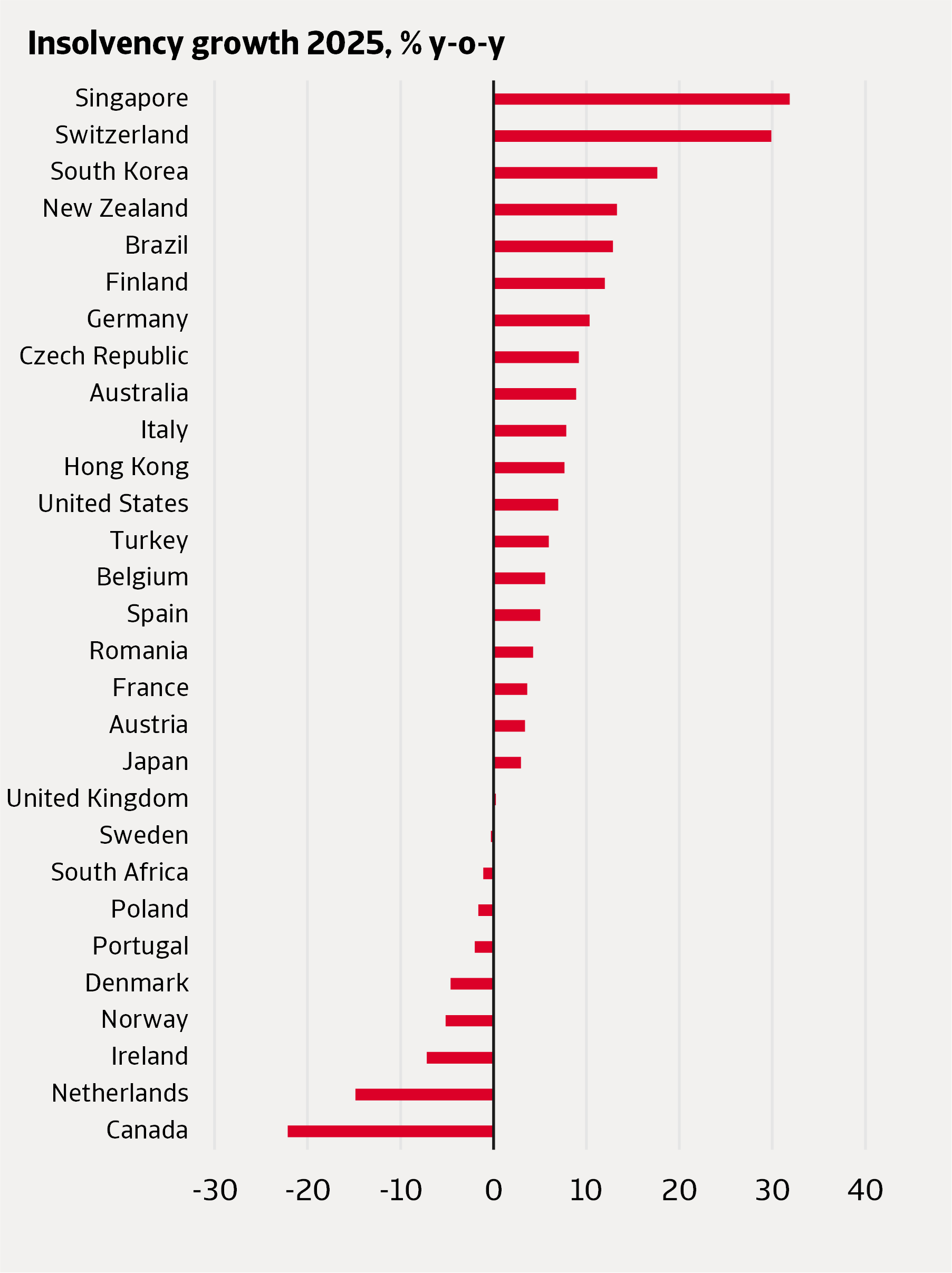

Globally, insolvencies increased significantly in 2025 at 5% year‑on‑year. Insolvencies rose in all three major regions. The slowest increase was in Europe at 4%, while North America experienced a slightly higher rise of 5%. Asia Pacific was clearly distinct from the other two, with an increase that was twice as large at 9%.

The increase in insolvencies in North America was driven by the rise in the US, where insolvencies surged by 7%, mostly in the second half of 2025. High interest rates, tighter lending and cost pressures increasingly weighed on companies’ financial positions. Canada, on the other hand, saw a sharp drop in insolvencies after the record high number in 2024. In 2024, Canadian insolvencies were historically high due to the deadline to repay loans from Covid‑related government programmes, alongside other economic factors such as high interest rates and high inflation. This was just a temporary surge in insolvencies as we now see a return to a structurally normal level. Monetary easing in Canada was steeper than in the US and the euro area, which may have contributed to a faster decrease in insolvencies.

In the largest European economies, we see an emerging pattern of slowing insolvency growth. In Germany, the pace of the rise in insolvencies slowed, and a stabilization emerged in the second half of 2025. Weak demand in export markets and high energy costs meant that insolvencies in Germany not only returned to their pre‑Covid level but exceeded it by a wide margin. Insolvencies stabilized in France, while they continued to increase in Italy. French companies are facing weak domestic demand and debt overhang, and insolvencies are at historically high levels. In Italy, on the other hand, insolvencies remain below their pre‑Covid level. A similar pattern of slowing insolvency growth was observed in Austria, Romania and Spain. Insolvencies in Spain remain high due to a combination of factors: the end of support measures, cost pressures and tighter lending conditions. The legal reform of 2022 in Spain also made it easier for companies to file for insolvency.

In several European countries, 2025 marked a turning point, with insolvencies no longer rising but starting to decrease. This was especially pronounced in Ireland and the Netherlands. Economic growth was strong in Ireland, which supported corporate recovery. In the Netherlands, a legal framework that was introduced in 2021 makes it easier for companies to restructure and settle their debts without entering a bankruptcy procedure. As a result, more Dutch firms chose to close without formal insolvency proceedings, and total company closures increased in 2025. Insolvencies in Norway, Portugal and Poland also fell slightly in 2025. Macroeconomic conditions were favorable in Norway and, while some sectors faced financial difficulties such as construction and hospitality, others performed particularly well, including energy and oil services. Insolvencies in the UK remained stable in 2025 after a slight decrease in 2024.

The situation in Asia-Pacific was the worst. Singapore, South Korea and New Zealand experienced some of the highest insolvency growth rates worldwide. Insolvencies in Singapore returned to their pre-Covid level, while in South Korea and New Zealand they exceeded the pre-Covid level by 145% and 64% respectively.

Figure 1: Insolvencies continued to rise in most markets in 2025

Source: Atradius

Companies in South Korea faced weak domestic demand. South Korean companies, especially SMEs, are highly leveraged and were heavily hit by high interest rates.

New Zealand enterprises were affected by weak economic conditions. Insolvencies in Hong Kong and Japan increased slower than in other Asian countries. Japanese companies experienced historically high insolvencies level due to weak sales, labor shortages and inputs cost increase due to weak yen. Many companies are facing excessive debts. Insolvencies in Australia continued to rise, despite historically high level. Insolvencies in the retail and transportation sectors were increasing faster than in other sectors.

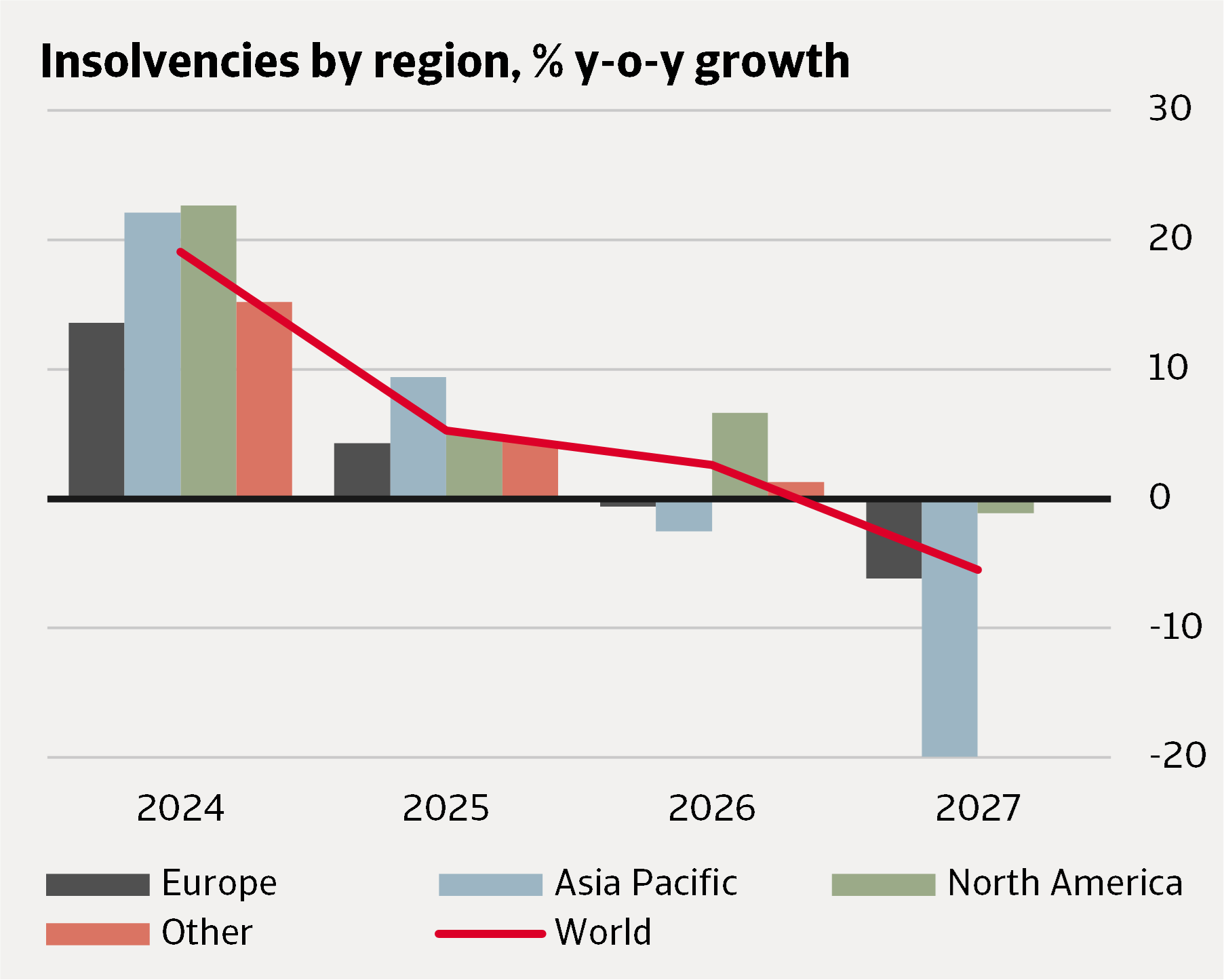

Globally, our expectation is that insolvencies will grow moderately by 3% in 2026, with signs of normalization to lower levels generally starting in the second half of 2026. This is a 6 percentage points upward revision compared to our October 2025 Insolvency Outlook, when we expected that insolvencies will start normalizing from early 2026.

The business climate will remain vulnerable in 2026 as the adverse conditions affecting companies are more persistent than we previously anticipated. Specifically, Covid-related tax debts, the rise in the input costs and trade tensions are all contributing to keeping overall insolvency levels high in 2026.

Our forecast is generally informed by the economic outlook of a given market and the most recent realization of insolvencies in the data. However, in cases where companies are affected by adverse conditions and insolvencies are abnormally high, we expect insolvency levels to return to pre‑pandemic levels by the end of 2027, adjusted for the difference in economic activity. We think that this is a natural benchmark to evaluate the normality level of insolvencies since the evolution of insolvencies after the pandemic has been a decline to abnormally low levels, driven by government support schemes, followed by an increase driven by higher interest rates, high input costs, and the withdrawal of government support. The degree of the increase in insolvencies in recent years differs by country, but for some countries insolvencies have clearly reached an abnormally high level. For these countries, we expect a normalization to lower insolvency levels in 2027.

Figure 2 presents our forecasts aggregated globally and at the regional level. The only region where insolvencies show a convincing decline in 2026 is Asia Pacific. Early 2026 data suggests that insolvencies have reached their peak and that the trend for the rest of the year is downwards. North America shows a substantial increase of 7%, driven by a challenging economic climate marked by trade tariffs. Europe shows approximately no change on aggregate, as the picture is balanced between countries that continue to see a rise in insolvencies and others where the adjustment has started. By 2027, the decline in insolvencies from a relatively high level continues in Asia Pacific and starts in Europe, while North America remains almost unchanged.

Figure 2: In most regions, a downward normalization of insolvencies is postponed to 2027

Source: Atradius

The following subsections detail key developments in each region, with annual growth rates for 2026 and 2027 shown in Figure 3 for all monitored markets.

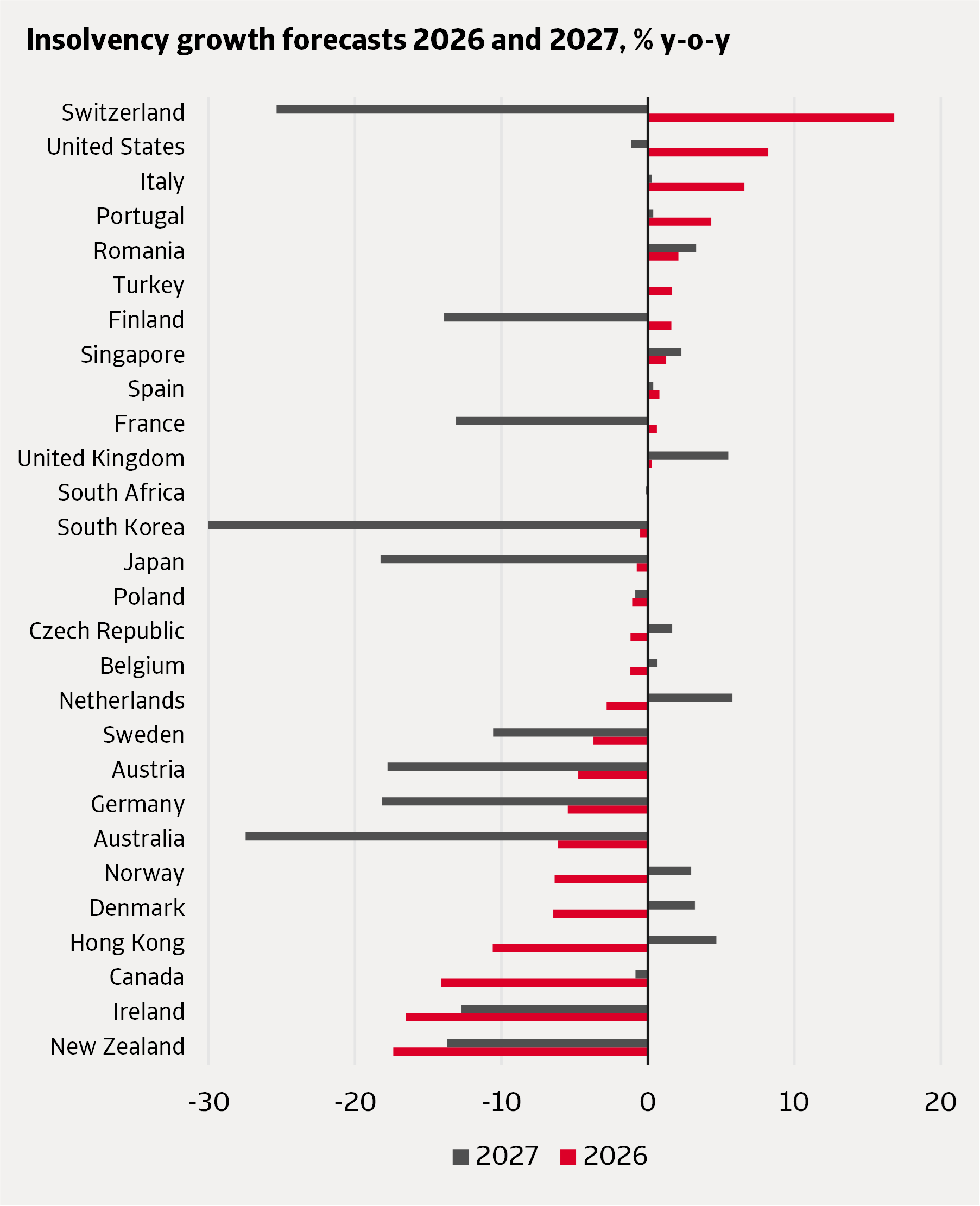

In the United States, insolvencies are projected to rise by 8% in 2026 and remain almost unchanged for 2027. This forecast is mostly in line to what we expected in our October 2025 Insolvency Outlook. The economic climate remains challenging for companies, with high trade tariffs and increased policy uncertainty. This is confirmed by early insolvency data for 2026 that shows a continuation of the high levels seen at the end of 2025. Looking ahead to 2027, economic growth is anticipated to recover slightly, thus, leading to a relative stabilization of insolvencies.

In Canada, we expect insolvencies to continue their downward adjustment throughout 2026, leading to a 14% decrease in the full year. They are expected to stay almost unchanged in 2027. This may come as counterintuitive, since the Canadian economy was exposed to trade tariffs with the US. Canada faced a steep rise in insolvencies in 2024, triggered by delayed filings by small businesses following the end of pandemic-era support. Corporate insolvencies settled back to more typical levels in 2025, a trend that recent data shows continued in early 2026. In 2027, we think insolvencies will remain stable at levels slightly above normality, reflecting ongoing pressure on companies from adverse factors.

Figure 3: Insolvency growth forecasts 2026 and 2027, % year-on-year

Source: Atradius

Europe presents a mixed outlook in 2026, with some countries still experiencing increases in insolvencies, while others experience a decrease in insolvencies. We expect the highest increases to occur in Switzerland, Italy and Portugal, while the most significant decreases are likely to occur in Ireland, Denmark and Norway.

In Switzerland, insolvencies are expected to increase by 17% in 2026, reaching a level double as high as what was normal pre-pandemic. The abnormally high level of insolvencies could be linked to changes in the bankruptcy legislation that requires public institutions to initiate bankruptcy proceedings against companies in case these have unpaid debts. Moreover, in 2026 companies will have additional pressure from the weakening of the domestic economy and of external demand from neighbouring eurozone countries. We expect that the downward adjustment of insolvencies will start gradually from the second half of 2026, leading to a 25% decrease for 2027.

In Italy, insolvencies are expected to increase by 7% in 2026, reflecting the continuation of an upward adjustment from low levels after the pandemic. By 2027 we believe this adjustment will be over, implying approximately no change in insolvency levels. Although the insolvency data indicates a relatively low default risk, this should be regarded with caution as there is evidence of an increase in out-of-court proceedings following a legislation change from late 2021.

In Portugal, insolvencies are expected to increase by 4% in 2026, mainly reflecting a base effect relative to the low levels in the first part of 2025. Given that economic growth is expected to stay close to its long-run trend, we believe insolvencies will stabilise in 2027.

Looking at the countries where insolvencies decrease in 2026, Ireland stands out with a 17% decline. This relatively strong decrease is expected, since late 2025 already shows signs that normalisation from high insolvency levels has begun. For 2027, we expect insolvency levels to revert to pre‑pandemic values, implying a further decrease of 13%.

We find a similar pattern in Sweden, although the recent normalisation in insolvencies has been more limited. Extrapolating this trend forward, we obtain a decrease of 4% in 2026 and 11% in 2027.

Decreases in insolvencies in 2026 are also expected in Denmark and Norway, both by 6%, and in the Netherlands by 3%. Unlike the previous group of countries, insolvencies at the end of 2025 were relatively low compared with pre‑pandemic levels. We interpret this as a sign that companies in these countries showed greater resilience to global economic headwinds. However, with subdued economic growth and negative shocks, our forecast implies a partial reversal to higher levels in 2027. For the Netherlands, we foresee an increase in insolvencies of 6% in 2027, while for Denmark and Norway we expect a 3% increase.

Most monitored markets in the Asia Pacific region are expected to see decreases in insolvencies in 2026, reflecting an overall downward adjustment from the historically high level in 2025.

The largest adjustments are expected for New Zealand, with decreases of 17% in 2026 and 14% in 2027. Our forecast is influenced by the recent drop in insolvencies in Q1 of 2026, which suggests that the downward adjustment has already begun.

We also expect a significant contraction in insolvencies of 10% in 2026 for Hong Kong. For 2027, however, we forecast an increase of 5%, reflecting a partial reversal of the sudden drop in insolvency levels in early 2026.

By comparison, in Australia, Japan and South Korea, where we see no clear signs of normalisation in the recent data, we expect insolvencies to stay high until mid-2026. As Figure 3 shows, in annual terms this implies that most of the downward adjustment occurs in 2027.

Finally, for Singapore we expect a relatively mild increase in insolvencies for 2026 and 2027. We consider that here insolvencies will remain relatively stable since they have mostly finished their upward adjustment from the low levels following the pandemic levels and the most recent data shows no signs of an upward trend.