Atradius Atrium

Get direct access to your policy information, credit limit application tools and insights.

United States

United States

Australia

Australia

Austria

Austria

Belgium

Belgium

Brazil

Brazil

Bulgaria

Bulgaria

Canada

Canada

China

China

Czech Republic

Czech Republic

Denmark

Denmark

Finland

Finland

France

France

Germany

Germany

Greece

Greece

Hong Kong SAR

Hong Kong SAR

Hungary

Hungary

India

India

Ireland

Ireland

Italy

Italy

Japan

Japan

Lithuania

Lithuania

Mexico

Mexico

Netherlands

Netherlands

New Zealand

New Zealand

Norway

Norway

Poland

Poland

Portugal

Portugal

Romania

Romania

Singapore

Singapore

Slovakia

Slovakia

Slovenia

Slovenia

Spain

Spain

Sweden

Sweden

Switzerland

Switzerland

Turkey

Turkey

United Arab Emirates

United Arab Emirates

United Kingdom

United States

United Kingdom

United States

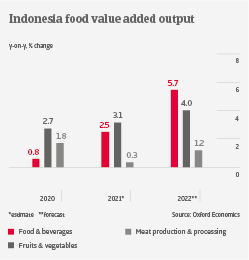

The Indonesian food & beverages sector remained resilient in 2020 and 2021, and value added output increased 0.8% and 2.5% respectively. The beverages and dairy segments show robust growth rates. Prices for meat remain stable, as the government has increased import quotas. However, consumer demand for fruits and vegetables is impacted by rising sales prices. Online groceries and food delivery businesses gained momentum during the pandemic, while hospitality and food services benefited from the partial easing of restrictions in late 2021 as the vaccination rollout gained momentum.

The Indonesian food & beverages sector remained resilient in 2020 and 2021, and value added output increased 0.8% and 2.5% respectively. The beverages and dairy segments show robust growth rates. Prices for meat remain stable, as the government has increased import quotas. However, consumer demand for fruits and vegetables is impacted by rising sales prices. Online groceries and food delivery businesses gained momentum during the pandemic, while hospitality and food services benefited from the partial easing of restrictions in late 2021 as the vaccination rollout gained momentum.

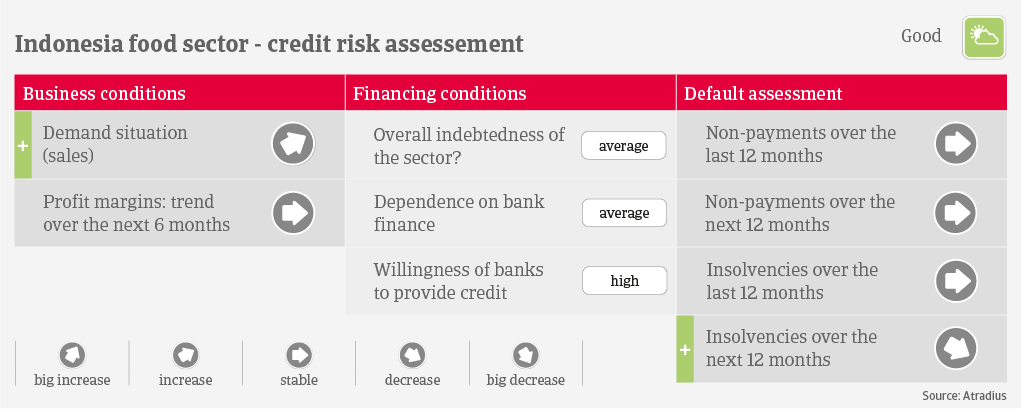

We expect that profit margins of most businesses will remain stable this year. The impact of globally rising energy and commodity prices has been limited so far. The government sets energy prices, and most agricultural products needed for further processing are produced in Indonesia. Rising labour costs are not an issue, as labour is widely available and the government regulates wages. That said, price increases in some segments with higher import dependency (dairy, meat) could not be avoided.

Across the industry the gearing of businesses is manageable, and banks are generally willing to lend to food & beverages companies. Payments in the sector take about 30-60 days on average. Payment behaviour has been good over the past couple of years, and we expect this positive trend to continue. Due to the still robust performance during the pandemic and ongoing demand growth, we expect protracted defaults and insolvencies to level off in 2022, or even to decrease by about 5%-10%.

Our underwriting stance is mainly open for food processors and producers, in particular if businesses are part of a larger group. However, we are more cautious with highly leveraged companies. We maintain a neutral approach for food services and retail. In particular, food services and related hospitality still face the downside risk of another tightening of restrictions should coronavirus cases surge again.