Atradius Atrium

Get direct access to your policy information, credit limit application tools and insights.

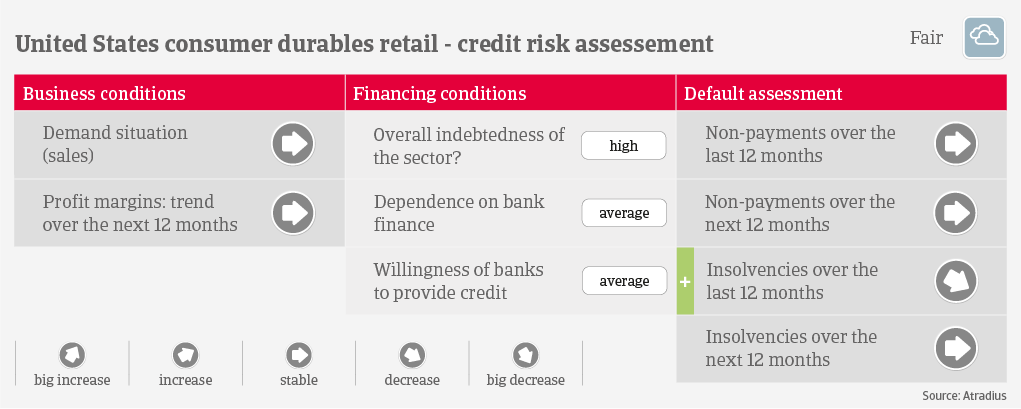

United States

United States

Australia

Australia

Austria

Austria

Belgium

Belgium

Brazil

Brazil

Bulgaria

Bulgaria

Canada

Canada

China

China

Czech Republic

Czech Republic

Denmark

Denmark

Finland

Finland

France

France

Germany

Germany

Greece

Greece

Hong Kong SAR

Hong Kong SAR

Hungary

Hungary

India

India

Ireland

Ireland

Italy

Italy

Japan

Japan

Lithuania

Lithuania

Mexico

Mexico

Netherlands

Netherlands

New Zealand

New Zealand

Norway

Norway

Poland

Poland

Portugal

Portugal

Romania

Romania

Singapore

Singapore

Slovakia

Slovakia

Slovenia

Slovenia

Spain

Spain

Sweden

Sweden

Switzerland

Switzerland

Turkey

Turkey

United Arab Emirates

United Arab Emirates

United Kingdom

United States

United Kingdom

United States

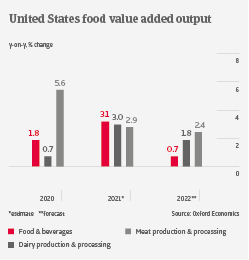

US food & beverages value added output is forecast to grow by about 1% in 2022, after increasing 3.1% in 2021 and 1.8% in 2020. The food retail segment benefited from higher sales over the past 24 months, but competition remains fierce and margins tight. In the food services segment a rebound is underway, but many businesses still struggle to absorb the sharp decrease in demand from hospitality seen in 2020 and H1 of 2021. The current spread of the Omicron variant remains a downside risk for the ongoing recovery.

Production costs have increased across all subsectors, due surging prices for commodities, transportation bottlenecks and labour shortage. Additionally, droughts in central and western states could adversely affect production and margins in the fruit and vegetables subsector. While the margins of food producers and processors have been impacted by higher input costs, both are in general able to pass on a large share of those costs to wholesalers/retailers and end-customers. This has resulted in the highest food price inflation since 2008 (up 6.3% year-on-year in December 2021). We expect that food prices will remain elevated until supply constraints ease in H2 of 2022.

Access to external financing is not an issue for food & beverages businesses. Many are private equity-owned and therefore highly leveraged, using credit lines for working capital. Ongoing mergers and acquisitions in the industry are also a reason for high debt levels. Payments in the sector take about 30 days on average, and the amount of payment delays and business failures has not increased 2021. We expect no deterioration in 2022.

Next to food retail, our underwriting stance is open for beverages, as most businesses in this segment show a solid performance and sufficient liquidity. We are neutral for the dairy and meat subsectors, where higher operating and production costs have an impact on margins. We are more restrictive regarding food services, as this segment is highly susceptible to the spread of the Omicron variant and subsequent repercussions for hospitality.