Atradius Atrium

Get direct access to your policy information, credit limit application tools and insights.

United States

United States

Australia

Australia

Austria

Austria

Belgium

Belgium

Brazil

Brazil

Bulgaria

Bulgaria

Canada

Canada

China

China

Czech Republic

Czech Republic

Denmark

Denmark

Finland

Finland

France

France

Germany

Germany

Greece

Greece

Hong Kong SAR

Hong Kong SAR

Hungary

Hungary

India

India

Ireland

Ireland

Italy

Italy

Japan

Japan

Lithuania

Lithuania

Mexico

Mexico

Netherlands

Netherlands

New Zealand

New Zealand

Norway

Norway

Poland

Poland

Portugal

Portugal

Romania

Romania

Singapore

Singapore

Slovakia

Slovakia

Slovenia

Slovenia

Spain

Spain

Sweden

Sweden

Switzerland

Switzerland

Turkey

Turkey

United Kingdom

United States

United Kingdom

United States

trade stock market economy (image)")

For many years, the economies in Asia have been the main growth engine of the world economy. Next to the big economies of China and India, the Southeast Asian countries have made strong contributions to global GDP growth. Although domestic demand continues to be strong in these economies, this year several downside risks appear to cloud the growth outlook for the region.

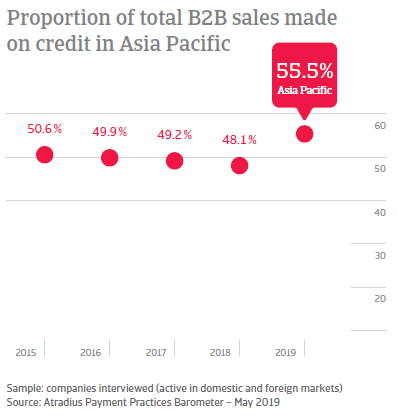

Survey findings highlight that respondents place more emphasis on the use of trade credit to maintain their competitiveness and gain market share than one year ago. This is a logical reaction to the current more challenging business and trade environment. With 71.5% of the total value of sales to B2B customers made on credit (up from 47.7% last year), Australia lead the way in Asia Pacific in terms of the use of trade credit in B2B transactions. Japan (67.2%) and Singapore (65.7%) follow. At the lower end of the scale, the 42.8% average recorded in Taiwan, stands out as the lowest in Asia Pacific. It is worth highlighting the growing trend in using trade credit in B2B transactions in China, where 44.3% of the total value of respondents’ B2B sales was on credit terms (up from 43.0% in 2018 and from 41.9% in 2017).

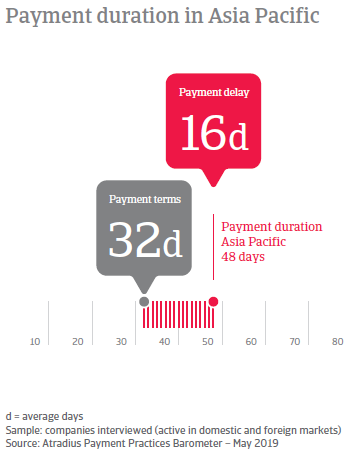

Despite being more inclined to offer trade credit to B2B customers than in the past, respondents in Asia Pacific do not appear similarly inclined to extend looser payment terms. This reflects clear recognition of the risks associated with credit sales and the more challenging trade environment. Survey findings reveal that respondents from Australia set the shortest payment terms (averaging 24 days from the invoice date). Longer payment terms are seen from respondents in the region averaging 26 days in China to 45 days in Taiwan. Taiwan’s average is well above the 32 days average for the region. Of note, Indonesia stands out as the country where average payment terms (at 34 days) are markedly longer this year than in last year’s survey (on average 11 days longer). This may reflect a need to loosen terms on export sales, to limit the fall off in export demand.

Despite being more inclined to offer trade credit to B2B customers than in the past, respondents in Asia Pacific do not appear similarly inclined to extend looser payment terms. This reflects clear recognition of the risks associated with credit sales and the more challenging trade environment. Survey findings reveal that respondents from Australia set the shortest payment terms (averaging 24 days from the invoice date). Longer payment terms are seen from respondents in the region averaging 26 days in China to 45 days in Taiwan. Taiwan’s average is well above the 32 days average for the region. Of note, Indonesia stands out as the country where average payment terms (at 34 days) are markedly longer this year than in last year’s survey (on average 11 days longer). This may reflect a need to loosen terms on export sales, to limit the fall off in export demand.

Survey findings in Asia Pacific reveal that, in addition to the short payment terms commented on earlier, businesses’ credit management policies include a mix of credit management tools and activities. The assessment of the creditworthiness of the buyer, prior to making any trade credit decision, plays a key role in the credit policies of respondents. Survey data highlight that respondents from Singapore (53%) and China (51%) do this significantly more often than their Asia Pacific peers do (39%). Reserving against bad debts, whose purpose is to offset potentially inaccurate screening of the buyer’s financial position, is the second most often used credit management tool in Asia Pacific. Respondents from Taiwan (42%) and Indonesia (41%) are notably more active on this front than their peers (33%). While there appears to be a strong focus on credit management in Asia Pacific, it is striking that a sizeable proportion of respondents in the region stated they do not have a strategic approach to credit management. This is the case in Australia (26% of respondents) and Japan (20%), compared to 10% at a regional level.

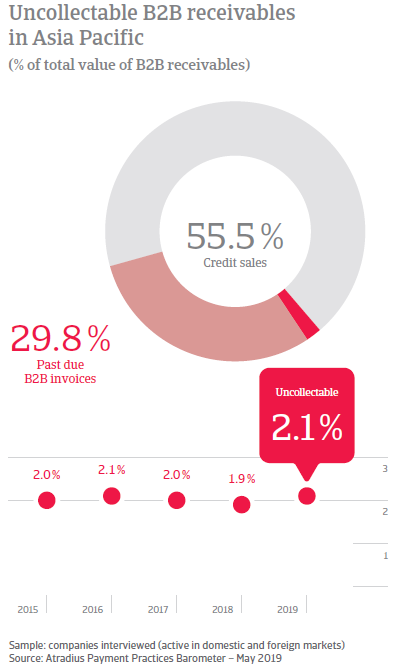

Survey findings reveal that, on average, respondents in Asia Pacific are converting past due invoices into cash in 48 days this year (seven days earlier than last year). On average, overdue invoices are collected within two weeks of the invoice due date. Despite this notable improvement in invoice to cash turnaround, on average, 29.8% of the total value of B2B invoices issued by survey respondents in Asia Pacific is reported to be past due. This percentage ranges from a high of 39.0% in India, to a low of 13.2% in Japan.

In order to remain financially sound and avoid liquidity issues caused by payment defaults of customers, many respondents in Asia Pacific (41%) said they had to delay payment of invoices to their own suppliers. This was most often the case for respondents from India (51%), followed by those from Indonesia (46%), China (45%) and Hong Kong (44%). 39% of respondents in Asia Pacific took corrective measures to safeguard cash flow. This figure climbs to a high of 49% of respondents in India and 45% in both Singapore and Indonesia. On the negative side, receivables that were written off as uncollectable in Asia Pacific increased to an average of 2.1% of the total value of B2B sales on credit (up from 1.9% last year). This suggests that businesses are less successful in collecting invoices than last year, but also that the business environment is deteriorating.

Almost half of respondents in Asia Pacific (47%) do not expect payment practices of B2B customers to change over the coming months. 22% anticipate an improvement, while 31% expect a worsening in the form of an increase in late payments, particularly in long overdue invoices (more than 90 days overdue). This will negatively affect DSO. Most concerned about this are respondents from India (52%), followed by those from Indonesia (35%) Singapore (33%) and China (31%). To protect their business against the risk of payment default by their B2B customers, 46% of respondents in Asia Pacific will check their buyers’ creditworthiness more regularly. This is particularly the case for respondents in Taiwan (60%) and China (57%). 44% of respondents in the region plan on increasing bad debt reserves, the highest percentage of which are in Hong Kong (49%) and Australia (47%). Respondents from China, Hong Kong (around 50% each) and Australia (47%) reported they will increase use of credit insurance to protect their business from the risk of payment defaults by customers.

For more insights into the overall payment practices in each of the countries surveyed in Asia Pacific, please refer to the respective country reports, which form, along with the regional report, the 2019 edition of the Atradius Payment Practices Barometer for Asia Pacific.

By country / business sector / business size

• Australia – Respondents from the manufacturing and consumer durables sectors gave the longest, and those from the services and agri-food sectors the shortest, average payment terms to their B2B customers. Based on survey findings, trade credit risk is high in the wholesale/retail/distribution and consumer durables sectors. The consumer durables sector, along with the agri-food sector, recorded the highest proportion of uncollectable receivables.

By business size, large enterprises appear to be the hardest hit, and micro enterprises the least impacted, by payment defaults from B2B customers. Despite their short credit terms, SMEs recorded the highest proportion of uncollectable invoices.

• China – The services and ICT/electronics sectors, as well as SMEs set the longest average payment terms for their B2B customers. The shortest terms were recorded in the wholesale/retail/distribution and consumer durables sectors. Survey findings reveal that trade credit risk is highest in the manufacturing, machines and construction sectors.

The proportion of uncollectable receivables is highest in the manufacturing and consumer durables sectors. SMEs took the longest to collect overdue invoices, also recording the highest rate of uncollectable B2B receivables.

• Hong Kong - Average payment terms are longest in the manufacturing and consumer durables sectors, shortest in the services and construction sectors. The financial impact of late payments is highest in the wholesale/retail/distribution and the consumer durables sectors. The percentage of bad debts written off as uncollectable is highest in the manufacturing and consumer durables sectors. SMEs extended the most relaxed average payment terms to B2B customers and waited the longest to turn overdue invoices into cash. Bad debts are written off at highest rate in large enterprises.

• India - Average payment terms are longest in the services, consumer durables and construction sectors. The wholesale/retail/distribution, agri-food and ICT/electronics sectors recorded the shortest payment terms. The financial impact of late payments was most acutely felt in the services and ICT/electronics sectors, while the highest percentage of bad debts written off as uncollectable was observed in the services and ICT/electronics sectors.

On average, SMEs extended the most relaxed payment terms to B2B customers, and micro-enterprises waited the longest to turn overdue invoices into cash. Bad debts are written off at the highest rate in large enterprises.

• Indonesia –The manufacturing and consumer durables sectors set the longest average payment terms. The shortest terms are in the services and construction sectors.

The consumer durables sector takes the longest to turn past due invoices into cash, while the rate of uncollectable receivables is highest in the construction and lowest in the services sector. Micro-enterprises extended the most relaxed payment terms to B2B customers, while large enterprises recorded an increase in invoices paid late from B2B customers and the largest proportion of uncollectable receivables.

• Japan – Respondents from the manufacturing and machines sectors extended the longest average payment terms to their B2B customers. The shortest terms are set in the wholesale/retail/distribution and consumer durables sectors. The financial impact of late payments is highest in the manufacturing and construction sectors, while the percentage of bad debts written off as uncollectable is highest in the wholesale/retail/distribution and ICT/electronics sectors.

SMEs extended the most relaxed average payment terms to B2B customers, and recorded the longest invoice to cash turnaround. Large enterprises have the highest rate of bad debts written off as uncollectable.

• Singapore - Average payment terms are longest in the machines and ICT/electronics sectors, and shortest in the wholesale/retail/distribution and construction sectors. The ICT/electronics sector is hardest hit by late payments of B2B customers, while the rate of uncollectable B2B receivables is highest in the construction and lowest in the services sector. Micro-enterprises extended the most relaxed payment terms, while large enterprises recorded an increase in invoices paid late by B2B customers, and the highest rate of uncollectable receivables.

• Taiwan - Average payment terms are longest in the services and ICT/Electronics sectors, and shortest in the wholesale/retail/distribution and consumer durables sectors. Over the past year, the speed of payment from B2B customers of respondents improved the most in the services and the ICT/Electronics sectors. The wholesale/retail/distribution and consumer durables sectors have the highest proportion of uncollectable receivables.

Large enterprises extended the longest, and micro-enterprises the shortest average payment terms. B2B customers of both large and micro-enterprises pay faster than last year. Large enterprises recorded the highest rate of uncollectable receivables.